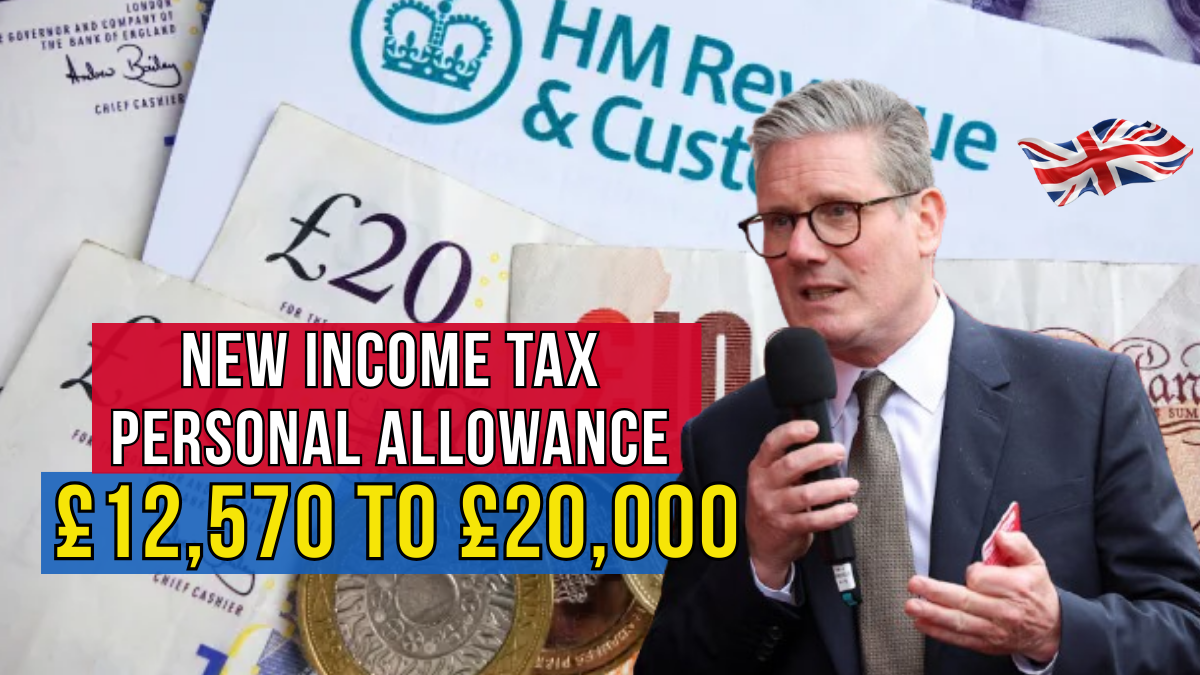

The debate over UK income tax reform has intensified in 2025 after a widely supported petition called for the Personal Allowance (the amount of income you can earn before paying tax) to be raised from £12,570 to £20,000.

This proposal, started by campaigner Alan David Frost, has captured the attention of the public and Parliament alike. By September 1, 2025, the petition had received more than 281,000 signatures, far surpassing the 100,000 needed for consideration in Parliament.

Supporters argue that such a rise would ease the burden on low-income households and pensioners, giving them more disposable income during a cost-of-living crisis. However, the government has expressed concerns over affordability, warning that the change could cost the Treasury £40–50 billion per year.

What Is the Personal Allowance?

The Personal Allowance is the annual income you can earn before paying income tax. Currently, the allowance stands at £12,570 and has been frozen since 2021.

Critics argue that, due to inflation and wage growth, freezing the allowance has led to fiscal drag, where more people are pulled into paying tax or into higher tax bands.

Quick Overview: Current vs Proposed Personal Allowance

Aspect |

Current (£12,570) |

Proposed (£20,000) |

|---|---|---|

Tax-free income |

£12,570 |

£20,000 |

Pensioners affected |

Many taxed on State Pension |

Most pensions tax-free |

Savings for middle earners |

Limited |

Up to £1,486 yearly |

Treasury revenue impact |

Stable |

£40–50bn loss |

Inflation risk |

Stable |

Possible rise in consumer prices |

Political pressure |

Moderate |

Very high with 281k+ signatures |

Debate status |

Frozen since 2021 |

Awaiting parliamentary debate |

Official portal |

Why Raise the Personal Allowance to £20,000?

Supporters of the proposal believe the change would have significant benefits, including:

- Immediate relief for low earners – Millions of workers would stop paying income tax altogether.

- Support for pensioners – Most pensioners would see their State Pension income fall below the tax threshold.

- Economic boost – More disposable income could encourage higher consumer spending.

- Reduced reliance on benefits – By keeping more earnings, families may need less state support.

Campaigners see the move as a way of delivering fairness and ensuring people keep more of what they earn.

Government Response – September 2025 Update

Despite public pressure, the government has rejected raising the allowance to £20,000 at this stage. In its official response, ministers emphasised that such a rise would:

- Create a £40–50 billion annual hole in Treasury finances.

- Limit funding for public services like the NHS, schools, and social care.

- Increase pressure on national debt and fiscal responsibility goals.

While rejecting the immediate change, the government noted that tax policy is reviewed regularly and that future Budgets and Autumn Statements remain opportunities to revisit the issue.

Who Would Benefit the Most?

1. Low-Income Workers

Workers earning below £20,000 annually would no longer pay income tax, saving hundreds of pounds each year.

2. Pensioners

Currently, many pensioners pay tax on their State Pension. Raising the allowance would make most pensioners tax-free, reducing financial pressure during retirement.

3. Middle-Income Earners

People earning more than £20,000 would also benefit, saving up to £1,486 per year, depending on their income and tax band.

Current UK Rules on Personal Allowance

The Personal Allowance is not applied equally to all taxpayers:

- Earnings over £100,000 – allowance is reduced by £1 for every £2 earned above this limit.

- Earnings above £125,140 – no allowance at all.

- Marriage Allowance – couples can transfer up to 10% of their allowance.

- Born before 6 April 1935 – may qualify for the Married Couple’s Allowance for additional relief.

Challenges of Raising the Personal Allowance

While attractive to households, the proposal has significant obstacles:

- Revenue Loss – estimated £40–50 billion shortfall, which would need to be covered by cuts or other tax rises.

- Risk of Inflation – more disposable income could fuel higher prices, counteracting the benefit.

- Public Services Pressure – less tax revenue could impact the NHS, education, and welfare programs.

- Potential Alternative Taxes – VAT, National Insurance, or capital taxes might be raised to balance the books.

What Happens Next?

The petition process in Parliament follows clear steps:

- At 10,000 signatures, the government must issue a formal response.

- At 100,000 signatures, the issue qualifies for parliamentary debate.

- With 281,000+ signatures, MPs are expected to debate the proposal, but legislation remains uncertain.

International Comparison

Other countries have higher personal allowances or thresholds, for example:

- United States: First $14,600 (~£11,600) is tax-free, but broader deductions exist.

- Germany: Tax-free allowance is around €11,600 (~£9,900).

- Australia: Tax-free threshold is AUD 18,200 (~£9,400).

The UK’s proposed £20,000 allowance would rank among the most generous in developed economies.

FAQs About Personal Allowance Debate 2025

Q1: What is the current UK Personal Allowance?

A: £12,570 per year.

Q2: Has the government agreed to raise it to £20,000?

A: No. The government has rejected the proposal due to high fiscal costs.

Q3: Who would benefit most from the rise?

A: Low-income workers, pensioners, and middle earners up to £50,000 would gain the most.

Q4: When was the Personal Allowance last increased?

A: It has been frozen since 2021.

Q5: Where can I check official updates?

A: Visit the government’s official portal: www.gov.uk.

Final Thoughts

The call to raise the UK Personal Allowance from £12,570 to £20,000 has gained remarkable public momentum, showing the depth of concern over the cost-of-living crisis.

While the government has rejected the proposal for now, the sheer scale of support over 281,000 signatures ensures the issue will remain central to political debate in the coming months.

For households, the key takeaway is that although the allowance is frozen, any changes will be announced through official government fiscal events. Pensioners and low-income workers stand to gain the most if the allowance is eventually raised.